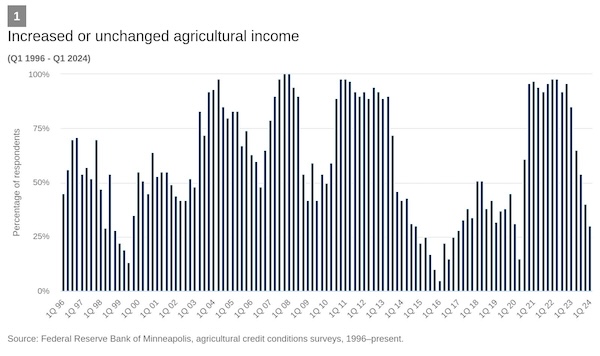

| I’m worried about farmland prices if real interest rates stay higher for longer and crop prices drift back down to pre-Covid levels (i.e. corn sub-$4.00, soybeans sub-$10, wheat sub-$6). I’m not saying this will happen for certain, but if it does I have to imagine it heavily weighs on farmland prices. The good news (perhaps I should say kind of good news) is the fact we have more and more buyers entering the space and creating increased demand for farmland. That’s not good news, however, if you are looking to be a buyer, but the increase in overall demand by those looking to purchase land for solar farms, data centers, housing developments, and pension funds adds another layer of support underneath the farmland market. In other words, there are a lot more buyers of farmland for various reasons than at any point in history. These additional buyers not only drive prices higher but can also help soften the blow when the market pulls back. Below is what some of the regional Fed Banks are reporting. Recent updates from regional Federal Reserve banks highlight the challenging conditions US farmers face this year amid lower crop prices, high operating costs, and tight credit. The three Fed districts that cover the major US crop growing regions include the Chicago Fed, which covers the 7th District (Illinois, Indiana, Michigan, and Wisconsin); the Minneapolis Fed serves the 9th district (Minnesota, Montana, North and South Dakota, 26 counties in northwestern Wisconsin, and the Upper Peninsula of Michigan); while the Kansas City Fed serves the 10th District (Missouri, Nebraska, Kansas, Oklahoma, Wyoming, Colorado, and northern New Mexico). All three regional Fed banks say falling farm income has led to an increase in demand for loans. The banks also highlighted the strength of the cattle market as an exception to overall low commodity prices. The Kansas City Fed noted that credit conditions in Q1 2024 tightened comparatively more in states with greater reliance on crop revenues and less in more cattle-heavy areas, a trend witnessed across the other two districts as well. The Chicago Fed’s Ag Letter is available HERE; the Minneapolis Fed Ag Credit Conditions Survey is HERE; and the Kansas City Fed Ag Credit Survey is HERE. Below are some other highlights: Farm Income and Credit Conditions: Bankers surveyed in all three ag districts indicate that farm incomes fell further in the first quarter of the year as loan demand climbed. The KC Fed says as lenders entered the renewal period for annual operating lines, loan denials were very limited but many reported an uptick in carryover debt and loan restructuring to meet liquidity needs. All three districts have seen increased demand for non-real-estate loans relative to a year ago while the availability of funds declined. Collateral requirements have also increased at many agricultural banks across all three districts. There has also been a small decline in repayments reported by ag banks as falling incomes continue to stretch budgets. Land Values and Cash Rents: Farmland values and cash rents were up across all three Fed districts in Q1 2024, though the gains varied. 7th: The Chicago Fed notes that the +4% year-over-year increase in 7th district farmland values was the smallest since Q3 2020. Adjusted for inflation, the year-over-year gain in 7th District farmland values for the first quarter of 2024 was just above +1%, marking the 16th consecutive quarter of real year-over-year growth. The Chicago Fed also noted that survey participants said the share of acres purchased by farmers was down relative to last year, “implying that the share of acres purchased by investors was edging up in parts of the District.” Cash rental rates for District farm acres increased by +2% percent from 2023 to 2024, which was the fourth positive yearly change in a row. However, after being adjusted for inflation with the Personal Consumption Expenditures Price Index (PCEPI), District cash rental rates were actually down -1% in 2024 from the previous year. Nearly 60% of 7th District ag bankers considered farmland to be overvalued. Even so, responding bankers generally expected farmland values to be unchanged in the second quarter of 2024: 7 percent of these bankers forecasted agricultural land values to increase, 76 percent forecasted them to be stable, and 17 percent forecasted them to decrease. |

9th: The growth in land values seen over the past several years continued but tapered off, and cash rents also grew, according to the Minneapolis Fed. Ninth District nonirrigated cropland values increased by more than +3% on average from the first quarter of 2023. Irrigated cropland values rose by nearly +10% from a year ago, while ranch- and pastureland values edged up +6%. The district average cash rent for nonirrigated land rose by just +1% from a year ago. Rents for irrigated land increased slightly more than +1%, while ranchland rents increased +7%. |

| 10th: The Kansas City fed says farmland values remained firm in Q1 with average gains across all types growing by +5% or more. Following tepid growth throughout 2023, cash rents on all types of land rose modestly in the first quarter. Lenders in the region expected both farmland values and cash rents to be flat going forward. Looking ahead to the next three months, 75% of respondents expected the value of nonirrigated farmland to be unchanged compared with a year ago and 85% expected cash rents to be unchanged. Equal shares of the remaining respondents anticipated increases and decreases in the coming months, highlighting expectations of generally stable conditions for farmland markets. |